Uber’s SpotHero Acquisition Is an Autonomous Infrastructure Bet | PA Dispatch No. 12

A quick view of this week’s shifts in platforms, valuations, and AI adoption. Numbers, context, and curated reads you can use.

With the announcement of Uber buying SpotHero, it first reads like a logical adjacency:

Ride-hailing platform buys parking marketplace

Urban mobility meets urban parking

Cross-sell airport rides with airport parking

All of this is true, but if you zoom out and view this through the lens of autonomous vehicles, fleet utilization, and unit economics, this is not simply a parking acquisition, it’s an infrastructure acquisition. More specifically it’s an AV parking and fleet management play.

Reframing Parking in an AV World

In a human-driver rideshare world parking is a friction. Drivers cruise, double-park, idle, and occassionally pay for short-term parking. It’s inefficient but it’s not Uber or the 1P provider’s problem since the driver bears the cost.

In an AV world, the fleet provider beats the cost whether it’s Uber, Tesla, or Waymo. The moment vehicles become autonomous and fleet owned (or fleet-managed), parking shifts form a nuisance to a core cost center.

If an AV sits idle 6 hours per day and urban structured parking averages $20–$40 per night, that’s $7,000–$14,000 annually per vehicle in parking alone. Across 20,000 vehicles, that’s a $140M–$280M annual cost center. Based on conversations I’ve had around trying to build out AV specific depots at scale, that can come down to $80-120 per vehicle per month, but that’s assuming opportunistic asset availability of 1,000+ vehicle parking lots.

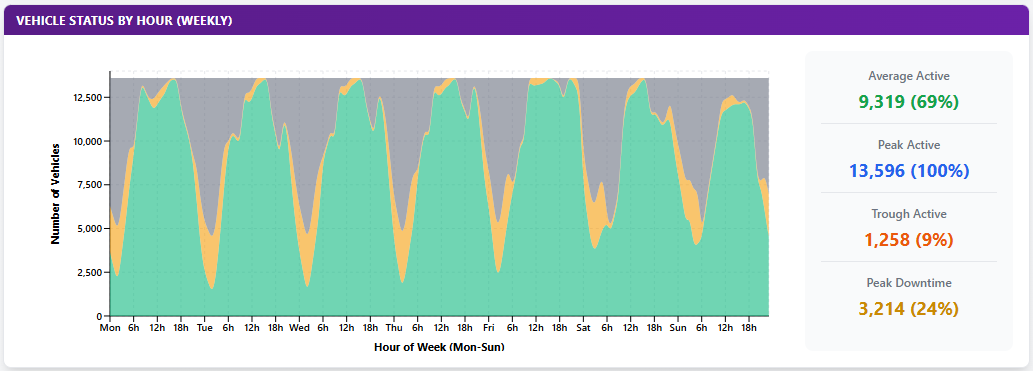

Awhile back I put together a fleet optimizer system and one of the charts is vehicle status by hour:

But let’s try to shift our mind into 3D and think about how this demand is not only distributed across hours, but across geography. In the future when there are 14,000 AVs driving around Los Angeles where do they go during periods of latent demand? The obvious first answer is charging and cleaning depots. We’ll likely need 10-20 depots geographically distributed around a city with 500-1,500 parking spots each. But that’s naturally a bit less efficient as there’ll be significant deadhead driving to get to depots and there’s also the reality that there just isn’t enough large scale parking available in most urban environments.

How do you optimize depot location, sizing, and availability while working within physical constraints? I think SpotHero can be a big help with this.

How SpotHero Can Help with AV Fleet Management

After a Waymo or Nuro AV drops off a rider and it’s 2am and demand is latent what does it do next? It can’t circle endlessly, it can’t double-park forever, and what if it’s clean and mostly charged already? Does it warrant driving to a depot? What if the depot is 25 miles away and Uber’s demand forecasting knows that there’ll be demand at 6am for rides in that location?

SpotHero can help provide ad-hoc on-demand parking for downtime for AVs to help optimize vehicle location and reduce costs. If Waymo’s are just randomly parking on the street during latent demand there’s the obvious risk to damage, but also think about the political or publicity issues. I lived in Somerville, MA outside of Boston for a decade and if you’re familiar at all with the area there’s a big reputation for people slashing tires or keying cars if you park in the “wrong spot” or you’re not “from the neighborhood”.

I think cities will continue to restrict curb space, regulate AV staging, impose idle restrictions, and generally crack down if we get anywhere near the scale forcasted for AV robotaxis. This makes parking a potentially valuable asset.

The optimal solution very well may be matching up periods of low demand for parking spot asset owners with AVs that need a place to sit and wait for additional demand. If you’re a business or real estate owner in a quasi-urban area and your operating hours are 9am to 5pm and you have 5-10 parking spots, those can be available through SpotHero to AV fleets just as latent/spare demand during periods of your choosing. It’s a win-win-win for the parking owner, the AV fleet, and SpotHero/Uber.

This doesn’t solve the charging and cleaning issue, that’ll need to be solved through actual depots with significant infrastructure, but SpotHero and Uber can help dial up utilization and fleet optimization through ad-hoc parking.

If Uber can integrate SpotHero inventory directly into fleet routing algorithms, parking stops become programmable. Vehicles can stage exactly where demand forecasting predicts a surge. Parking becomes part of dispatch logic.

Performance & Valuation Snapshot

Note: Email renders these as images, click through for interactive filters or view on Platform Aeronaut.

What I Read This Week

Waymo expands robotaxi service to 10 U.S. cities: Waymo added Dallas, Houston, San Antonio, and Orlando, aiming to scale toward 1M+ weekly paid trips by end of 2026.

DoorDash posts strong demand but warns of heavy 2026 spend: Q4 orders and revenue rose sharply; the company says unifying DoorDash/Wolt/Deliveroo onto one platform will be expensive and pressure near-term profitability.

Booking CEO details the “connected trip” vision: Emphasis on seamless travel (automatic updates when disruptions hit) with AI as the glue across trip components.

Uber to acquire parking-reservations app SpotHero: Uber adds in-app parking (commuters/events/airports) as part of its “super app” push; SpotHero operates in 400+ cities.

Expedia’s annual filing calls out “agentic AI” as a competitive threat: Expedia explicitly flags AI-driven travel search/booking as a risk from faster-moving entrants.

Winter disruptions renew focus on “agentic travel” workflows: Piece argues MCP-style coordination could help agents carry structured traveler constraints (identity/loyalty/payment) across systems.

Transcript Highlights

Airbnb (ABNB) - Q4 2025 Earnings Call

A custom AI customer support agent is resolving roughly a third (about 30%) of support issues in North America and is reported to reduce resolution times.

Brazil moved from a top-ten market to a top-five market and was the second largest contributor to first-time bookers in Q4 behind the U.S.

AI-enabled product experiments (including AI search and sponsored listings tests) are underway, but no material sponsored advertising revenue is yet disclosed or banked into guidance.

Booking (BKNG) - Q4 2025 Earnings Call

Generative AI integration into customer service contributed to roughly a 10% decline in customer service costs per booking

Genius loyalty program Level 2 and 3 members represented over 30% of the active base at Booking.com and accounted for a high 50% share of room nights for the full year, up from the prior year.

Social media investment grew 13% year over year in 2025 as the company leaned into new social channels with attractive ROIs

Instacart (CART) - Q4 2025 Earnings Call

The 2025 new-customer cohort generated the largest GTV contribution since 2022 and cohorts are retaining at higher rates year over year.

Restaurant integrations (including with Uber Eats and Grubhub embedding) materially contributed to mix and small-basket growth.

Over the past year, average output per engineer is up nearly 40%.

The information presented in this newsletter is the opinion of the author and does not reflect the view of any other person or entity, including Altimeter Capital Management, LP (”Altimeter”). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for informational purposes and should not be construed as investment advice or an investment recommendation. Past performance is no guarantee of future performance. Altimeter is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. Altimeter and its clients trade in public securities and have made and/or may make investments in or investment decisions relating to the companies referenced herein. The views expressed herein are those of the author and not of Altimeter or its clients, which reserve the right to make investment decisions or engage in trading activity that would be (or could be construed as) consistent and/or inconsistent with the views expressed herein.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

This acquisition doesn't make any sense to me on the consumer side, parking is literally the alternative to Uber.

But I am totally with you on the AV fleet side. In a robotaxi world, distributed parking garages could serve as staging, charging, and overflow depots, effectively becoming a flexible supply buffer that Uber can price and allocate dynamically between consumers and fleet operations.