JSX: Challenger or Regulatory Ambiguity?

JetsuiteX (JSX) has been the subject of heightened scrutiny over whether they're a true challenger to the traditional airline model or just exploiting regulatory loopholes at the expense of safety

Last week twitter was in an uproar over start-up airline JSX (formerly JetSuiteX) being under attack by competitors and regulators. The issue is portrayed as regulatory capture by the big airlines trying to attack and destroy a service that customers (and especially Silicon Valley VCs) love. There’s a bit of a false comparison between what JSX is doing and what other startups have done in moving fast and breaking things (Uber, Lyft, etc) in that aviation is highly regulated for one singular reason (safety) as opposed to to maintain economic gates (taxi medallions).

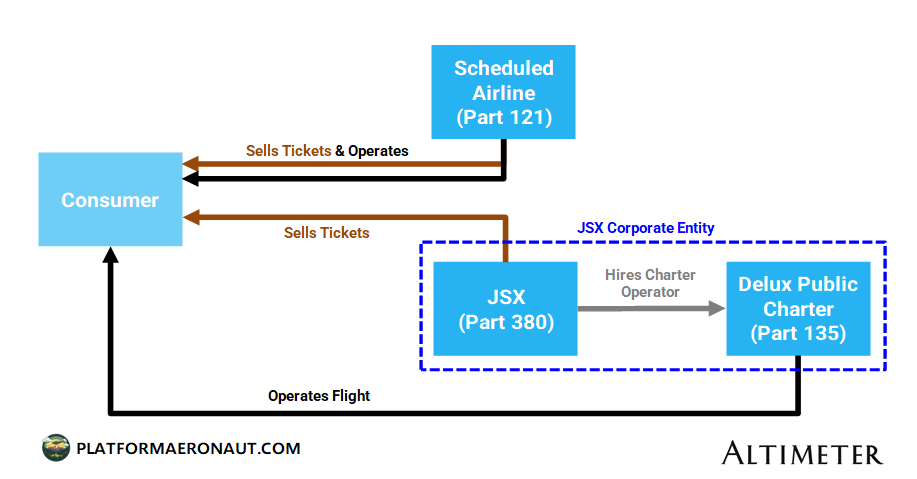

To give some background, JSX operates point-to-point flights in the US (and Mexico) that sells tickets directly to consumers and operates out of FBOs (no TSA security, no crowds, valet park and get on the plane within 20 minutes). They operate a fleet of Embraer 135 and 145 with 30 seats (E-135s usually operate with 37 seats and E-145s with 50).

The value proposition is you get to fly out of the private terminal with no security, roomier seats, complimentary cocktails & snacks, wi-fi, and no waiting for baggage claims while paying prices equivalent or less than the traditional carriers

But there’s a lot more detail to dive into on the state of JSX and whether it’s a true challenger being leaned into or whether it’s exploiting a regulatory loophole. At it’s core the issue comes down to FAA certification regulations. JSX operates under 14 CFR Part 135 which is focused on charter and commuter services, while the traditional airlines operate under 14 CFR Part 121 (Regularly Scheduled Air Carriers).

To give a sense of the high level size of JSX, for June 2023 they transported almost 67k passengers and are likely at a ball-park run-rate revenue of $150-160m/yr so they are no small potatoes. Given they are a Part 135/Part 380 operator, JSX doesn’t have to report nearly as many statistics on safety, delays, revenue, etc to the FAA or the DOT as Part 121 operators like UAL 0.00%↑ or JBLU 0.00%↑.

And if we look at JSX’s peer set you can see they’ve reached an unmatched scale among the Part 135 quasi-scheduled and commuter operators:

There is clearly consumer demand for the product especially in a post covid world. If I can pay the same (or less) than I would on a mainline carrier and avoid the airport chaos and TSA why wouldn’t I?

JSX Operating as a Charter Under Part 135

The crux of the issue at hand is that JSX is operating under Part 135 regulations as opposed to the more stringent Part 121 regulations for scheduled air carriers. The Air Line Pilots Association (ALPA) has called on the DOT to close the Part 135 loophole that JSX operates under:

“JSX simply is wrong. If it walks, talks, and quacks like a duck, it is a duck. Since JSX does in fact provide scheduled service, it should be deemed to do so, regardless of the fictitious regulatory disguise that it dons.”

Part 135: Charter Type Services

Part 135 operating certificates are intended for on-demand charter operations or commuter operations. The intention behind the guidelines are for air taxi services, private air charters, transactional private jets situations to have a separate certificate and requirements from typical scheduled airlines. Aircraft must have fewer than 30 passenger seats with a payload <7,500lbs.

Part 380: Public Charters

Part 380 is the set of regulations detailing how public charters can be managed, tickets sold, and flights operated. What Part 380 does is essentially outline how public charter tickets are sold.

Loophole

The FAA filed a Notice of Intent to Consider Revisions to the Regulatory Definitions of “On-Demand Operation”, “Supplemental Operation” and “Scheduled Operation” with the following background:

[Part 380] is an economic regulation administered by the Department of Transportation. Currently, under 14 CFR 110.2 of FAA’s safety regulations, public charters operated under the terms of 14 CFR part 380 may be conducted as “on-demand operations” if the aircraft operator is using airplanes, including turbo-jet powered airplanes, with 30 or fewer passenger seats. On-demand operations must be conducted under the operating rules in 14 CFR part 135. See, 14 CFR 119.21 (a)(5) and 135.1(a)(1). Similarly, public charter operations are excepted from the § 110.2 definition of “scheduled operation” and are included in the definition of “supplemental operation” regardless of whether such operator offers in advance to the public the departure location, departure time, and arrival location of the flight. But for the part 380 exceptions in § 110.2, public charter operators would be required to comply with the operating rules 4 applicable to their operations based on the same criteria as all other air carriers and commercial operators, i.e., 14 CFR part 121.

Essentially what is happening is that you have an economic regulation from the DOT (Part 380) that is superceding and exempting some Part 135 airline operators from the safety requirements normally required based on the type of flying they’re doing. The FAA continues:

If the FAA were to remove the exceptions, operators would then conduct public charter flights under the operating part applicable to their operation based on the same criteria that apply to all other non-part 380 operators, including the size and complexity of aircraft they operate and the frequency of flights

How is JSX Using the Regulations?

JSX uses the Part 380 loophole by saying that it’s merely operating scheduled charters. JSX sells the tickets under Part 380 and contracts with Delux Public Charter to actually operate the scheduled service. Delux Public Charter is 100% owned and controlled by the JSX corporate entity and is 100% captive and there is no real benefit to setting up the business this way except to utilize the Part 135/380 exemption.

The end result of this proposed rulemaking is that JSX and other operators using this loophole would have to adjust and most likely transition to a Part 121 certificate similar to every other scheduled airline.

Why Would JSX Use Part 135?

Costs, Costs, and Costs (and flexibility)

The regulatory burden of operating under Part 121 can’t be understated when compared to Part 135. Part 121 requires higher levels of record keeping, maintenance, managerial oversight, data collection by the FAA/DOT, customer service, pilot training, and a slew of other things.

The clearest difference is on pilot training and safety. After the 2009 Colgan Air Flight 3407 crash the minimum hours for a pilot at Part 121 operators was raised from 250 to 1,500 hours due to training concerns. Part 135 operators like JSX still retain the 250 hour minimum. Additionally Part 121 operators have a 65 year old mandatory retirement age, while 1/3 of JSX pilots are over age 65. The European Union has continued to keep their mandatory retirement age of 65 due to concerns over sudden flight crew incapacitation.

Additionally JSX and Part 135 operators can fly their pilots harder and longer, flight hours for Part 135 cannot exceed:

1,200 hours in any calendar year (vs 1,000 for Part 121)

120 hours in any calendar month (vs 100 for Part 121)

34 hours in any consecutive 7 days (vs 30 for Part 121)

Given the business model and network of JSX I severely doubt that they’re anywhere close to either Part 121 or Part 135 maximums for pilot hours, but it’s theoretically possible for others utilizing this model.

And although JSX has policies in their Operator-Participant Contract, many of the the DOT Flyer’s Rights that many consumers are used to do not apply to charter operators.

And although more difficult to estimate I have to imagine that the savings as a result of not paying the airport and contractors for gates, baggage services, check-in desks, management real estate and likely meaningfully lower landing fees have to be significant.

Simply put, Part 135 allows JSX to operate with lower cost pilots, fewer regulations and overhead expenses, and fewer requirements for consumer protection. Additionally it allows them to hire pilots that can’t work elsewhere either due to mandatory retirement ages or not enough flying hours so JSX isn’t subject to the same pilot shortages as peers.

Why is this issue being raised?

I think the FAA notice to review this was brought up for a few reasons:

Scale of JSX has reached a level that attracts attention. They’re no longer an experiment as they’re hitting larger revenue numbers and likely close to P/L breakeven. Aviation is a cutthroat business and it’s not difficult to see it presenting a threat to scheduled carriers, and the pilot union ALPA is fighting to protect it’s own members (and likely a desire to expand to cover JSX pilots)

SkyWest Applied to do the same thing with their old 50-seaters and serve EAS markets. This is likely a way for SkyWest to a) utilize older aircraft that are uneconomical and b) operate regional flights for United at breakeven that can be handsomely profitable with EAS subsidies.

Why is it a Problem?

The reality is that it’s more of a competitive issue than it is a true safety issue. Competitors view JSX as utilizing the Part 380/135 loophole against the spirit of the law and JSX views it as fully complying with current laws and regulations.

On Ben Baldanza’s Airlines Confidential podcast, JSX CEO Alex Wilcox mentioned that 1/3 of pilots have >15,000 hours, 1/3 are under 2,000 and the remainder are chosing to work at JSX for the lifestyle (sleeping at home everynight instead of in a hotel).

JSX says they go above and beyond the Part 135 requirements for safety in terms of FOQA, ASAP, and Safety Management Systems and are essentially on-par with Part 121 requirements.

Tickers Mentioned: UAL 0.00%↑ AAL 0.00%↑ DAL 0.00%↑ JBLU 0.00%↑ ULCC 0.00%↑ ALGT 0.00%↑ ALK 0.00%↑ LUV 0.00%↑ SKYW 0.00%↑ MESA 0.00%↑ SAVE 0.00%↑ UBER 0.00%↑ LYFT 0.00%↑

Resources:

The information presented in this newsletter is the opinion of the author and does not necessarily reflect the view of any other person or entity, including Altimeter Capital Management, LP ("Altimeter"). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation. Past performance is no guarantee of future performance. Altimeter is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.