Travel Demand Reaction to War & Terrorism

In the wake of the terror attacks and subsequent war in Israel and Gaza this is a deep dive on the impact to travel demand as well as historical examples from previous events

The horrific attacks on Israel by Hamas are difficult to comprehend and the human suffering and pain in the region is unbearable and my heart goes out. Beyond that I wanted to take a step back and look at what the tangible tourism reaction is to both the events that have unfolded and look at how other recent events in history have impacted travel demand.

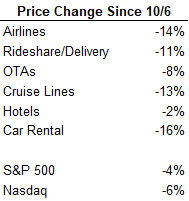

In terms of pure stock market reaction we’ve seen travel and leisure in general underperform versus the indicies. Not unexpected in a time of uncertainty in demand, a serious situation in the middle east, and a worldwide caution advisory from the US State Department:

Coming off covid revenge travel, weaker consumer health, a worldwide travel advisory, terrorist attacks in Israel, and a potential regional war in the middle east have had a meaningful impact on air travel bookings and demand.

First Step: Trip Cancellations

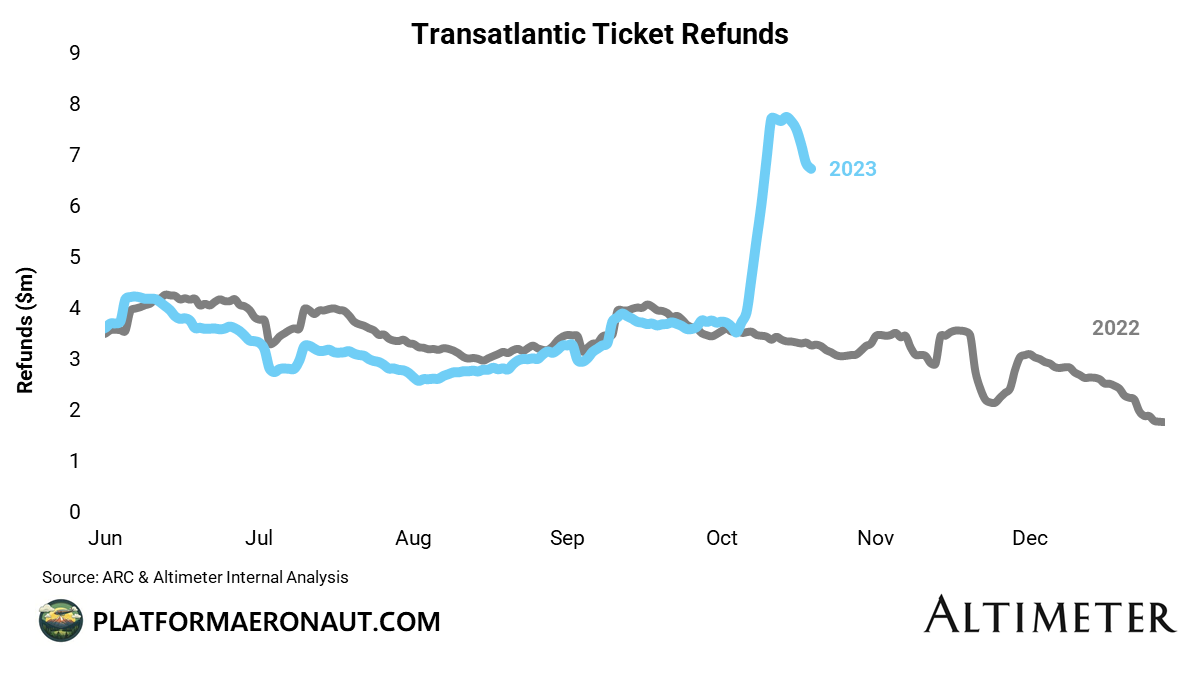

Almost always when there is war or terrorism events, travelers just cancel their trips, which is exactly what we’ve seen so far in transatlantic ticketing for air travel from the US. To give a sense of scale, this is approximately the same level of refunds on an absolute dollar basis that we saw in April 2020 at the height of the covid pandemic. Travel advisories and general anxiety and hesitation makes consumers just saw screw it, I’m not going on that vacation or business trip right now until things calm down or there is more clarity.

I think one interesting takeaway here is that despite Israel being around the same distance from Germany that Boston is from Denver (1,800 miles), we’re seeing cancellations impacting the entirety of the European continent.

Second Step: Weakness in New Bookings

Once you get through the initial panic and cancellations you just get a big drop in bookings because nobody is making new trips while so much is up in the air. There’s definitely some volatility in the chart above because post-labor day travel was already weaker (student loan repayments, kids back in school, and generally a trough leisure travel period with corporate still recovering). But we’ve seen 1,000bps+ of deceleration in US to Europe booking trends since the attacks in Israel despite significant physical distance between Israel and continental Europe.

Despite the reality of the data we’ve seen some pushback against the narrative of transatlantic weakness in demand on earnings calls:

UAL Q3 Call: “Demand for the Atlantic and the Pacific was truly outstanding and we see that trend continuing into the fourth quarter”

DAL Q3 Call: “The transatlantic remains very strong, driven by partner hubs and southern European leisure traffic performance.”

IAG Q3 Call: “But the impact for us is limited, because the flights to Cairo, Amman, and Israel for us is less than 1% of our total seats. So, it's true that it's too early to see or to conclude, if we are going to have any wider trend on implication. So, in general, bookings are in line with what we have in our forecast, but we are conscious about the situation that we have in the market”

Third Step: Recovery?

The big question is around recovery or normalization of demand. I wouldn’t expect demand for flights to Israel to recover anytime soon (United even put out two sets of guidance on whether TLV flights are suspended for one month or three months:

But I would anticipate some sort of recovery in demand to the rest of Europe if we get clarity on a potential regional war or terror attacks in large European cities (pending economic recession and consumer weakness offsetting that). If we look at a few examples of other recent attacks we generally see that demand recovers quickly (or isn’t really impacted at all)

2017 United Kingdom Terror Attacks

In the UK in 2017 we had a series of three high profile terrorist attacks:

Mar 2017: Vehicle and Knife Attack at Westminster

May 2017: Suicide Bomber at the Ariana Grande Concert at Manchester Arena

Jun 2017: London Bridge Vehicle and Knife Attack

In all three situations we saw temporary drops in demand for flights from the US to the United Kingdom, but once the news cycle was over we saw demand return to previous year-over-year trendlines within 2-3 weeks.

2017 Barcelona Terror Attacks

In August of 2017 there was an attack in Barcelona where vehicles were driven into pedestrians multiple times and an apartment was bombed followed by a manhunt. Looking at the demand data it’s pretty difficult to parse out the impact on travel bookings because it was already seeing deceleration from peak summer travel demand.

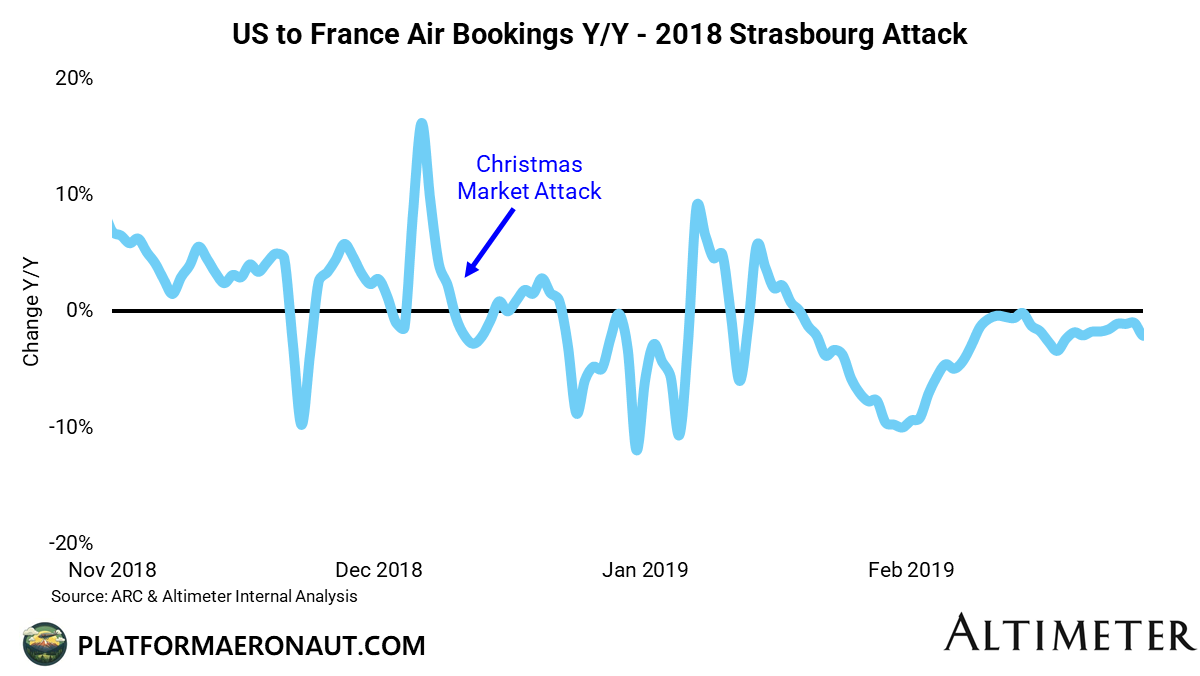

2018 Strasbourg Christmas Market Attack

In early December 2018 there was a Islamist/ISIL attack at a Christmas Market in Strasbourg France. From the chart above we can see a definite deceleration in demand from mid December until early January, after which trends appeared to normalize. This followed a pretty similar demand hit to recovery trend that we saw in the series of UK terrorism events a year earlier.

2022 Russian Invasion of Ukraine

Obviously demand to Russia and to Ukraine was (and remains) negatively impacted by the Russian invasion of Ukraine. But a better example for the impact on travel and tourism is the impact on neighboring countries so here is demand data from the US to Poland:

The absolute Y/Y trends are really high as it was in the midst of the recovery from covid, but we saw a big drop off right after the start of the invasion (similar in scale to what we’re seeing in the EU right now after the Israel-Hamas events). But fast forward 5-6 weeks and demand trends were back at previous levels. I’ll caveat this that there’s a significant probability that the peak in April 2022 is as a result of aid workers, military contractors, and other non-leisure travelers pouring into Poland to help support the situation in Ukraine.

Which Trendline will Demand Follow?

Looking at the historical comparisons, my expectation is that we’ll likely see a further drop in demand to Europe if/when Israel rolls into Gaza and then a slow recovery in the 4-5 weeks after that.

American (and global) travelers tend to have a short memory and normalize their behavior after the news cycle moves onto the next global event. Business travelers eventually need to go on the trips they’ve postponed. Unless we see a significant escalation of Israel-Hamas to a regional war including Hezbollah, Iran, and other neighbors, most likely we’ll be back to whatever the trend line should’ve been on transatlantic demand by mid-late November.

Tickers Mentioned: UAL 0.00%↑ DAL 0.00%↑ IAG 0.00%↑

Resources:

The information presented in this newsletter is the opinion of the author and does not necessarily reflect the view of any other person or entity, including Altimeter Capital Management, LP ("Altimeter"). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation. Past performance is no guarantee of future performance. Altimeter is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.