The State of Rideshare and Autonomous Vehicles

2025 is looking peak disruption for the human-centric rideshare model in the US with launches from Uber, Tesla, Waymo, Lyft, Mobileye, and Zoox.

If 2024 was the proof of concept for consumer’s interest and willingness to take autonomous rides with Waymo, 2025 will be the year of rapid rollout and proof of concept for the operating models themselves.

To start, here is a map of current and planned operations over the next 12-24months in the United States:

Today we have Waymo absolutely killing it in San Francisco, scaling in Los Angeles, and some questionable results in Phoenix with their Uber partnership. Tesla is planning their launch in Austin in June. Zoox is planning paid rides in Las Vegas. And Lyft and Mobileye are planning launches in Dallas and Atlanta, but not until 2026.

Waymo: Trying it all out

The strategic approach for Waymo is pretty clearly defined as trying out as many different business models as possible and see what works best.

1P in SF and Los Angeles with planned launches in Miami and San Diego

Waymo is operating exclusively first party in San Francisco and Los Angeles and as of the latest CPUC data through Aug 2024 they’re scaling rapidly, having gone from 20k rides per month in Aug 2023 to 500k rides per month in Aug 2024. Most worrying for Uber and Lyft is that per Yipit, Waymo market share in San Francisco is now equivalent to Lyft:

Uber and Lyft have claimed that they have not been overly impacted in SF with claims that a significant portion of Waymo bookings are either a) growing the market or b) AV tourists trying it out. To-date Waymo has been pricing the product at equivalent or slight premiums to UberX and Lyft to make up for the fact their vehicle cost is >$200k. But in 2025 and into 2026 through their partnership with Hyundai I’d expect that BOM cost to come materially down and for them to start pricing more aggressively versus Uber and Lyft.

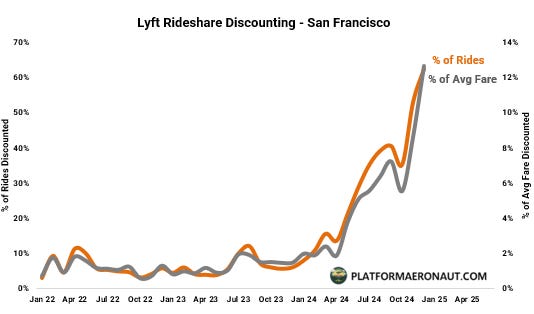

Given some of the data showing how much Lyft is discounting in San Francisco I find it hard to believe that Waymo isn’t having a material impact:

But that isn’t he main focus of this discussion so I’ll leave it at that. Through the 1P model Waymo utilizes you have a lot more control over the product, customer experience, and data collection, but the entire argument Uber makes is as follows:

Hence the Waymo partnership with Uber that exists in Phoenix and will launch in Atlanta and Austin.

In an interview that Ben Thompson at Stratechery did with Uber CEO Dara Khosrowshahi he said:

“…you need economics to work in order to scale, and in a world where certainly if the cost of capital is high and these cars are relatively expensive, the player that’s able to drive the highest utilization of these vehicles is going to have the lowest cost of capital. The player who works with us is going to be able to expand into every single market very, very quickly, will be first to market and being first to market matters, and I think those two elements, which is lowest cost of capital, ability to scale fastest, are going to play to the advantage that we bring in terms of being the best partner for AV in the world.”

My only push back to this is going back to the BOM argument that if a Waymo vehicle goes from $250k to $50k as they scale and you have BYD launching $10k EVs with autonomous capabilities at some point you may get autonomous vehicles that are so cheap you don’t need to be hyper focused on cost of capital for success.

Despite these upcoming partnered launches Waymo and Google CEO Sundar Pichai have talked publicly about Waymo being in 10+ cities by YE25 which implies incremental either 1P or partnered launches in cities like San Diego, Miami, Tampa, Orlando, Houston, etc.

Waymo & Uber in Phoenix

In Phoenix, Waymo has been working with Uber through a model where Uber is pre-purchasing supply to add to their existing rideshare network. This allows Waymo to test out the economics with Uber where Waymo is essentially just providing hours or miles to Uber and Uber can price and sell those however they please in combination with the human driver rideshare network.

The one concerning anecdote here that I’ve heard is that 50% of riders in Phoenix are choosing NOT to take a Waymo when given the option in the Uber app. I would expect some consumer hesitation outside of the SF tech mecca, but 50% is extremely high and hasn’t been coming down as operations have scaled.

Waymo & Uber in Atlanta

Although I view the operations in Phoenix as a good experiment, what unfolds in Atlanta will be a lot more interesting and relevant for the future of AV ridesharing. As far as I can tell, Waymo will just put some vehicles on a truck and they’ll be dropped off in Atlanta and it’s Uber’s responsibility from there. Of course Waymo will be operating the tech stack and providing some in-vehicle support, but Uber (and their fleet management partners) will be responsible for all other operations including pricing, cleaning, charging, etc.

The million dollar question for AV is whether you build to peak, average, or trough demand. Uber in their recent Q4 earnings presentation gave a chart of weekly variability in demand:

Theoretically this means either a human-AV hybrid rideshare network is required to service peak demand optimally or AV costs need to come down so much it doesn’t matter. Atlanta will be the testbed for this true hybrid market and whether Uber can optimize supply and demand to an extent that justifies partnership rather than Waymo just doing it themselves as 1P.

Tesla: A June 2025 launch after a decade of promises?

My colleague Freda Duan has extensively tweeted about the advancements made in FSD v13 and how close Tesla is to fully autonomous driving.

With the most important metric being the rate of improvement in disengagement ratio. The current expectation is that Tesla will launch robotaxi services in Austin in June 2025 after the launch of FSD v14 when the safety metrics are greater than those of a human driver:

How will a Tesla Robotaxi Network look at launch?

With the Cybercab a year+ away from full production I would expect a small launch similar to how Waymo and Cruise looked at the beginning in San Francisco. Think a dozen+ vehicles owned and operated by Tesla taking paying rides enabled through the Tesla app.

I would expect that if we see hundreds of rides safely completed that we’ll see this quickly scale. The significant advantage that Tesla has over Waymo or other competitors is vertical integration, low BOM costs, and a sense of strategic aggression given the importance of robotaxi to the Tesla stock.

There’s a big TBD on whether we will see the ability of current Tesla owners to put their vehicles on the rideshare network at launch, but I would expect a tightly contained beta launch with Tesla owned vehicles at the start and possibly a slow roll out to consumers over the course of the first year.

Will it work?

With low costs and classic Tesla attention grabbing I’d expect the initial metrics to be great. The trillion dollar question is whether it’ll be safe enough and how balanced will Tesla be on safety versus expansion. Any accidents like this Cybertruck running FSD v13.2.4 that ran into a lightpole will have severe consumer consequences on trust and safety.

If Tesla can prove it safely works and lidar is not required then the next battle is whether the cheaper BOM cost and inevitable lower per ride prices will more than offset the network demand challenges caused by both lack of human drivers for peak periods that Uber has and Elon’s D.C. adventures causing over a third of the country to boycott the Tesla brand. Incrementally, Tesla vehicle sales being down over 50% in most of Europe is pretty shocking and is bound to have an economic impact on the business.

Rats, Cats, and Dogs (Lyft, Mobileye, Zoox)

In a me-too moment, Lyft and Mobileye are partnering to launch in Atlanta and Dallas in 2026. The technology remains a complete question mark though and very few details having come out on safety, testing, or cost. I do find it hard to imagine that Mobileye is a relevant competitor to Waymo and Tesla, at least in the United States. And partnering with the laggard rideshare network in Lyft is unlikely to help.

Zoox is launching and aggressively testing in Las Vegas but again there’s been very little information about the safety and scalability or the cost.

At some point the challenge for all competitors to Waymo and Tesla is just the accelerating technology advantage for those two. The more vehicles on the road for Waymo and Tesla the better the technology will get and the cheaper the service will cost. Maybe in a period of ZIRP and wild VC investment you could jump start a new autonomous driving company successfullly or you could cold start something like X.ai if you’re Elon in the AI craze, but in 2025 we’ll see scaling network, economic, and technology advantages for the leaders.

Of course this is slightly different outside of the United States where there are different safety standards and economics. There are a number of Chinese AV players who are already successfully operating in China and it’ll be a competitive market globally among those players, Waymo, and Tesla. For the sake of brevity though I’m limiting this to just the United States for now.

Pace of Scaling

2025 might not be the peak for the pace of scaling for robotaxi or autonomous vehicles given production challenges, but if 2024 was about proving it worked and customers liked it then 2025 is about proving the economics of the business can work. By the end of this year we will have a much clearer picture on the following questions:

Uber and Lyft are required to faciliate demand?

Can Tesla run an independent rideshare network?

Is Tesla FSD v14 (or v15?) safe enough to run anywhere in the US commercially?

Is a Waymo-Uber partnership like in Phoenix where Uber just buys capacity from Waymo better or is Atlanta where Uber takes a lot more responsibility superior?

Uber CEO Dara Khosrowshahi on the Q4 earnings call claimed it’ll take until 2030 for AVs to have 10-15% market share of ridesharing. I think it’ll be faster but regardless, the impact to multiples and future expectations for all of the players will be represented in stock prices a lot sooner than that as we get more clarity on what works and what doesn’t.

Tickers Mentioned: UBER 0.00%↑ LYFT 0.00%↑ TSLA 0.00%↑ GOOGL 0.00%↑

The information presented in this newsletter is the opinion of the author and does not necessarily reflect the view of any other person or entity, including Altimeter Capital Management, LP ("Altimeter"). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation. Past performance is no guarantee of future performance. Altimeter is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

Quite a lot of new information in this post regarding Waymo. Specifically that they will be operating as a service in Las Vegas and San Diego. Up to now it had been reported these (along with New Orleans) were just road trip cities. Real service in 2025 in Miami as well as Vegas and San Diego is certainly more than was previously baked in as Miami was supposedly not live till 2026 with paid fares. Do you have any insight into whether Waymo will distribute these new cities with Depot Management by Moove (like Phoenix) or by Uber (like Austin & Atlanta)?

Regarding Tesla, do you expect them to launch with a small geofence in Austin? Will they launch without a safety-driver or will there be a period where it is safety-driver only? Since they are launching with 3 & Y supposedly, these will have steering wheels in them unlike the new Waymo Zeekr RT which will not have a steering wheel. Any insight to when we will see the no steering wheel Robotaxi providing paid fares?

Good summary. If Tesla FSD level 4 works, it will have a widespread impact on ride-hailing, oil, and auto industries. The market wants to pay a little for it now and more as we get some more evidence of it. How do you assess the risk/reward in Tesla stock?