Tech Dilution Role Model: BKNG

Easy to point out whose SBC is a disaster, who is the positive example?

TL;DR

There’s no shortage of companies with concerns about SBC and shareholder dilution (DASH, NET, ZM, CRM, META)

In search of the positive, we can hold up Booking BKNG 0.00%↑ as a role model for dilution.

Since 2009, BKNG has diluted shareholders <0.5%/yr while repurchasing shares with excess FCF.

Company DNA, management compensation alignment, international expansion and employee domicile all led to low dilution and high shareholder returns

In Search of a Savior: How can SBC and Dilution be Reasonable in Tech?

It’s frankly shocking to look at SBC and dilution at tech companies versus the rest of the SPY or IWM. Comparing a fast growing SaaS company to HD 0.00%↑ or V 0.00%↑ is a bit apples to oranges, but it’s intellectually honest to cross compare mature tech companies. To clarify, I think of a mature tech company through the lens of EBITDA and FCF margins. Nobody expects more mature tech (AAPL, BKNG, MSFT, ADBE, ORCL) margins to double.

What we see is despite many companies having already achieved long term run-rate margins, dilution levels are all over the place. To know what’s right you need some sort of framework for what dilution and SBC should look like.

Booking Holdings (BKNG)

There may be better examples out there and there are certainly larger ones (AAPL), but I posit BKNG as the best in class role model for tech companies. Let’s first look at what the historical dilution has been:

Methodology

Let’s break this down a little bit. My dilution calculations here are similar to the analysis done for Methodology #2 in my ridesharing dilution hell post. The numerator is the sum total of RSU, PSU, and stock options granted in a given year. The denominator is the basic shares outstanding at the start of the year plus RSUs, PSUs, and stock options outstanding at the same date. A kind of shorthand to get to diluted share count starting the year.

Three Phases of BKNG: Stock Options > RSUs > PSUs

Looking at the chart there’s three distinct phases to how BKNG used stock-based compensation.

2000-2004: Post IPO usage of stock options

Priceline IPO’ed in 1999 and like most companies of the period used stock options as the compensation for SBC to align employees, management, and shareholders. From 2000-2001 they were issuing net 3.3% of stock options a year. Out of the money expirations were low because the stock went from $8 at YE00 to $35 by YE01 (split adjusted)

In 2002 the stock went back to $10 and from an option perspective you actually saw dilution decline as worthless expiration of options exceeded new grants on a net basis. This ying/yang dilution trend continued through YE04 as the stock was volatile up and down and stock-based compensation was aligned with shareholders.

2005-2015: Conversion to RSUs

One underappreciated downside of stock options is that it often results in higher dilution than RSUs if your stock is a rocket ship up and to the right. An employee making $100k in salary and $40k/yr in stock options may be willing to accept only $25k of RSUs/yr as it’s “guaranteed”.

Like many peers, BKNG converted to RSUs in 2005 and stopped issuing stock options (except for some acquisitions that included the assumption of existing options). The end result is that dilution was elevated for the first couple years as employees were issued longer term vesting RSU packages, but dilution stepped down materially from 2009-2015 averaging only 0.4%/yr over the period.

2016-2022: Addition of PSUs

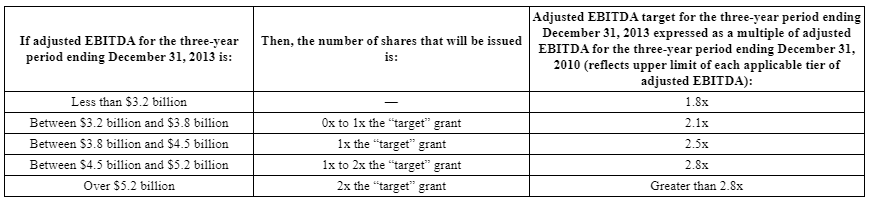

In 2016 the compensation committee on the board of directors introduced meaningful Performance Share Units (PSUs) as a component of the compensation for the C-suite. This is the natural next step where instead of just receiving cash or RSUs for achieving objectives, executives receive PSUs contingent on company performance. BKNGs was (and remains) significantly tied to relative share performance vs peers.

Through the use of PSUs greater alignment is achieved between shareholders and management and absolute RSU grants were reduced as they were re-allocated to PSUs. BKNG targets 75% of LT management compensation as PSUs and 25% RSUs.

How did BKNG Achieve This?

The big question is how did Booking manage to keep dilution so low when peers at META, GOOGL, AMZN, etc have seen significantly higher levels? Some of it is company DNA, some is geographic, some is performance driven, none of it is accidental.

Company DNA

Priceline (and subsequently Booking) has a lot of lore around the frugality of the management team including flying economy and barebones offices/benefits. Much of this can be traced to a company that in the dot-com boom and bust cycle went from flying high to death’s door. It instilled a focus on costs and discipline that remains today.

One barometer for the cost discipline of a company is how much they use adjusted metrics and whether stock-based compensation is included or excluded.

Compensate Executives on Metrics Including SBC

The majority of companies compensate their executives (and SVPs) on the basis of Adjusted EBITDA which often backs out stock-based compensation. For example EXPE backs out SBC so the incentive for management is to offload employee costs to RSUs as it doesn’t impact their own compensation. Wall street has historically overlooked dilution and focused on Adjusted EBITDA so this wasn’t an issue.

Compare this to BKNG where executives are compensated on “Compensation EBITDA” which is although is equivalent to their own “Adjusted EBITDA”, does not back out SBC.

International Expansion and Employee Base

Although originally a US based company with most of the GBV generated on Priceline.com, the acquisitions and growth at Agoda and Booking resulted in a company with a much more international employee base. Booking has ~21k employees at 3Q22 but only ~3.7k of those are located in the US.

Compare that to EXPE with ~15k employees of whom the majority are located in the US. This makes an enormous difference when it comes to 1) Base salary/benefit expense per employee and 2) SBC/RSU grants per employee.

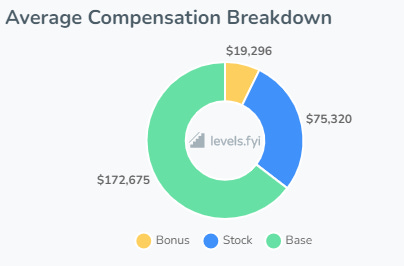

Let’s do a quick comparison between Booking engineers (most of whom are located in Amsterdam) and Uber engineers (who are mostly located in San Francisco). Different companies have different seniority tags making comparisons difficult, but these are for mid-level software engineers (think 3-6 years of experience)

The compensation is wildly different to the extent that not only is an engineer in the SF Bay area making a salary 70% higher, but their annual RSU value is 4x higher. Booking has benefited from being located outside the SF Bay Area and the US, and what we’re seeing the early signs of is companies hiring internationally and managing out US talent.

You can see this pertinently by going to the Uber Careers page where the majority of software job openings are located in India, Europe, South America, and other lower cost domiciles while the US is under a hiring freeze.

Can it Continue?

Booking has shown remarkable ability to remain disciplined on dilution and stock-based compensation. Some of it is geographic or company DNA, but a focus on shareholders and capital returns has created a machine that will likely continue to execute with low levels of dilution.

I expect to see companies choose one of two paths:

Path 1: Run the same playbook and dilute

If employees expect to receive their $50k of RSUs a year regardless of stock performance and senior management is compensated on financial metrics excluding SBC then trends will likely continue and dilution will remain high.

Path 2: Align with shareholders, find lower cost domiciles

Employees will either receive lower RSUs or ideally some sort of PSUs, companies will continue to exclusively hire internationally, and management compensation is aligned with actual shareholder returns inclusive of dilution.

The reality will be a mix of these, but it’ll take courage and commitment for any company willing to replicate what Booking has done the past 20 years.

Tickers Mentioned: BKNG 0.00%↑ EXPE 0.00%↑ UBER 0.00%↑ AAPL 0.00%↑ ABNB 0.00%↑ MSFT 0.00%↑ ADBE 0.00%↑ ORCL 0.00%↑

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.