Global Food Delivery: Normalization

From hyper-growth during covid to ugly comps in 2022, global food delivery is starting to see normalization on both growth and multiples in 2023

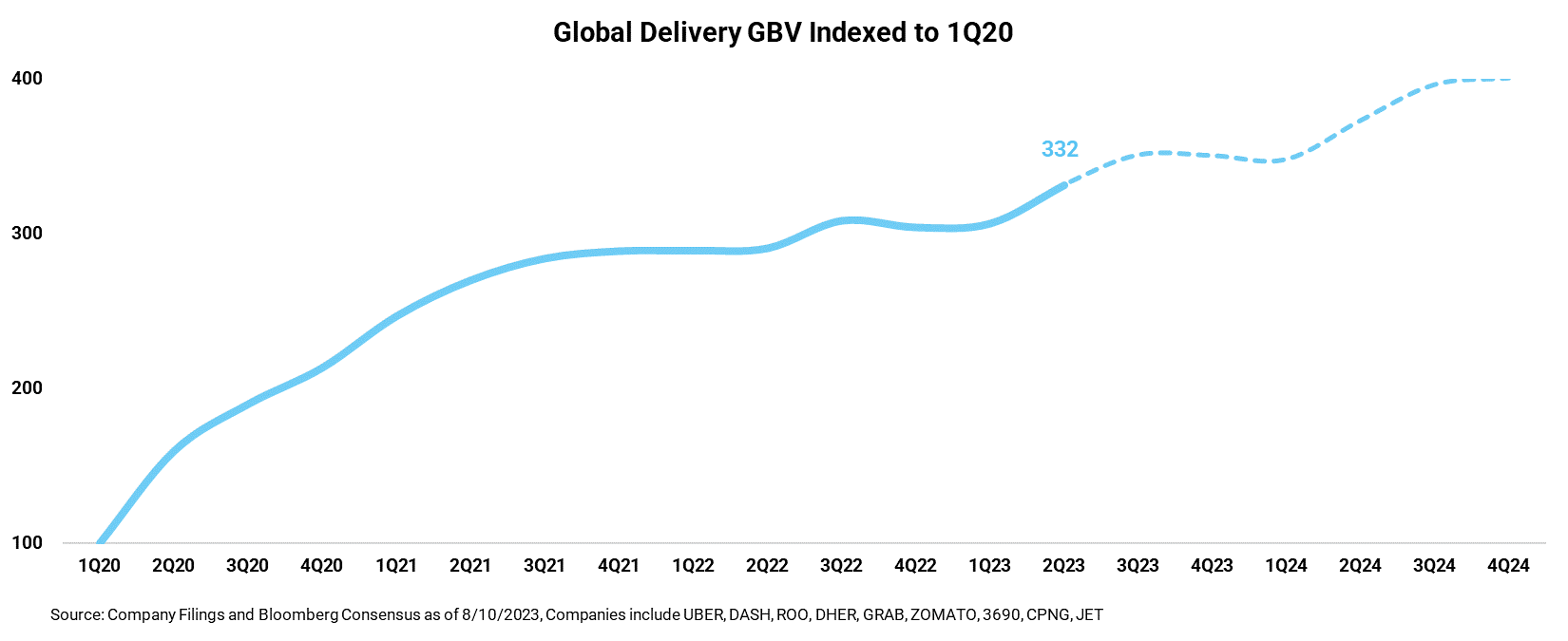

We’ve seen transformational growth in the global food delivery industry since 2019 as the Covid-19 pandemic raised DoorDash, Uber Eats, Deliveroo and others to household names. For context, in 2019 DoorDash did around $8B of GBV, 2021 they were 4x bigger at $42B, and consensus for 2024 is >7x bigger than 2019 at $65B.

Normalization of Growth

But with any good step change in demand there’s always a period of normalization, and for global food delivery it was tough. If we look at the period of 2Q22 to 1Q23 we went from triple and double digit GBV growth Y/Y to <10%

There were meaningful questions about the viability of the business. Profitability and FCF were not forthcoming and stocks were pummeled both from normalization of multiples, but also the reduction of future growth expectations. It’s easy to assume that the TAM had been fully penetrated as a result of the pandemic. The reality though is that the period of sub 10% growth was more normalization for a number of reasons:

Pandemic Cohorts: A number of the new platform users as a result of the pandemic were not long term users. Think of new Instacart users who signed up because they physically couldn’t leave home due to lockdowns. Or the elderly whose children signed them up for DoorDash.

Rationalized Marketing Spend: The biggest question for investors was whether these companies could ever reach meaningful profitability and the availability of free money and low interest rates enabled companies to continue growing at any cost. These were mostly empty calories aka customers who aren’t worth the LTV/CAC. Uber for example cut Sales & Marketing as a % of GBV from 5.2% in 2021 to 3.5% in 2Q23.

Pandemic Comps: Difficult comps are always a bit of bullshit, but there is some credence to the idea that 1Q23 was a “clean” quarter post-pandemic while 1Q22 was heavily impacted by the Omicron variant.

This is all most obvious when you drill down on the penetration of food delivery compared to overall food spending. This data is US specific but I would expect it’s fairly similar at a high level globally:

We saw clear elevation of delivery penetration as a % of overall US food spending during the pandemic and over the course of the past 18 months we’ve normalized at the pre-pandemic trendline of 12-13% penetration. Assuming that delivery penetration continues at the previous trendline, we could expect that double digit delivery growth is certainly achievable.

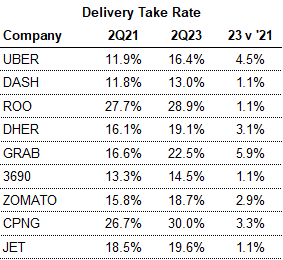

Global Take Rates Up

As the food delivery sector has normalized and businesses have gotten more fit (and focused on profitability), we’ve seen a meaningful increase in take rates for the platforms. For every $100 of GBV, the delivery companies were taking $14 as revenue early in the pandemic and today that is $16.

At first glance there is a concern raised that this isn’t sustainable but there’s a couple things that I’d call attention to:

Advertising: There’s a joke that on a long enough time frame every company becomes an advertising company. But we’ve seen advertising within food delivery become a meaningful portion of revenues (which skews the take-rate calculation). Uber Eats is at a $650m advertising run rate in 2Q23 versus $0 at the start of the pandemic.

Rationalization of Driver Supply: Tight labor markets, government stimulus, and a global pandemic all contributed to fewer people working as delivery drivers than there otherwise would’ve been. Over the past 18mo we’ve seen government stimulus evaporate, the pandemic disappear, and labor markets start to loosen very slowly. All of these help right size consumer and driver demand for working in food delivery and take rates will find an equilibrium.

Certainly I wouldn’t expect further upward revisions to global take rates (and in the chart above the future periods are Bloomberg/Visible Alpha consensus which don’t forecast significant further improvement.

Normalization of Multiples

I’ll caveat by saying that I know and fully acknowledge that LT EBITDA is a BS metric and was frequently used in 2021 to justify crazy multiples on both public and private businesses. This chart above is a little bit of a different take in that I used the consensus Bloomberg EBITDA multiples for 2025 and applied them backwards to estimate what the businesses and index overall would’ve theoretically been trading at on a longer term basis.

Things clearly got a little crazy during the pandemic and although delivery businesses weren’t the only ones (ahem *Software*), clearly valuing a food delivery business at 64x EV/EBITDA doesn’t make much sense.

We hit a low of 10.1x in late 2022 as GBV growth was slowing and profitability initiatives and rationlization of CAC hadn’t taken hold yet. Flash forward to today and we’re trading at 15.9x EV/EBITDA vs an ex-covid average of 18.3x. Doesn’t seem unreasonable for a sector growing at mid teens go-forward with improving profitability and FCF generation to be grading at a mid-teens EBITDA multiple.

Quotes on Normalization, Demand, Cohorts

Deliveroo:

“if you look at that also from a cohort perspective, which has been historical -- historically an important driver of growth, we're seeing some signs of stabilization there in terms of both frequency and max, and we see some opportunity ahead for those.”

Just Eat Takeaway:

“I think it's fair to say that Northern Europe, UK, and Ireland, that looks pretty normal to us that looks like we're back to relatively normal, normal seasonality. We still have a way to go. Of course, in North America and Southern Europe, but no the line share of our business looks like it's in very good shape.”

“And on the journey was more like the absolute churn numbers being elevated because you had a lot of money, new customers coming through COVID, but the relative churn number was actually doing very well.”

Delivery Hero:

“There are a number of other verticals (inaudible) either there is plenty of room to grow there, I think on the food side alone, there is plenty of room to grow by just maturing the cohorts and we see that cohorts improve over the year and as they age, I think there has been a little bit -- little bit affected by inflation and also prices.”

Uber:

“Generally, we're quite confident of delivery top-line growth going forward. And we think the penetration in these markets is very low. So in many of our developed markets, there are significant markets there, we've wired up anywhere from 20% of restaurants to call it 40% of restaurants in a particular market.”

Coupang:

“In the regions where we've launched our Eats benefit, we've already seen an 80% increase in total WOW members participating in Eats and a 20% increase in average WOW member spend on Eats. This has helped drive over 500 basis points of segment share gain in those regions.”

DoorDash:

“Consumer spending continues to be strong. The underlying cohorts continue to be very stable. That's what's giving us confidence to, first of all, bump up the GOV guide for the rest of the year.”

“We saw stronger and stronger cohort retention and growth. And that's, a combination of offering the best selection, quality, affordability.”

Zomato:

“I think the assumption here is that the worst is behind us in terms of the demand slowdown that we saw and from here on incrementally we should see that recover and hence we feel confident about being able to deliver this top line growth."

Tickers Mentioned: DASH 0.00%↑ UBER 0.00%↑ $3690, $JET $TKWY $ROO LYFT 0.00%↑ $ZOMATO GRAB 0.00%↑

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

Thanks Thomas. Great post and confirming the similar trend we’ve seen in ecommerce: reversion to the original trendline.

Two questions:

1. Do you project a difference in growth rate between restaurant delivery vs grocery delivery? Intuitively, I would say grocery delivery would grow faster because very few people actually love spending time at the grocery store while there are many other reasons to physically go to the restaurant besides consuming calories. But on the other hand, restaurant might be stealing more and more meals (out of the 21 meals you have in a week) away from grocery.

2. Dash, Uber, Instacart and Amazon all seem to be doing great. Do you see any of them uniquely positioned or doing better for the next few years?