Enterprise Software AI Pricing Power & Strategy

Every enterprise software company is coming out with AI tools and agents with a variety of pricing strategies. What is sustainable? What can capture true value? What is just ante into the game?

We’ve clearly moved into the Age of AI, and we’ve seen significant top-line growth for Nvidia and the rest of the hardware layer and some of that has continued onto the infrastructure layer with the hyperscalers and Databricks. The big question is when do we tangibly start to see ROI and returns from AI investments for the enterprise software layer?

I’ll caveat all this by saying unlike other posts this is fairly light on quantitative metrics and heavy on qualitative thoughts. I welcome comments on why you think I’m completely off base. It’s super early and strategies are constantly in flux but I’m making at attempt to review where things stand today.

Does Scale Matter in Age of AI?

One big topic is around does scale matter in the age of AI? The above chart is average software returns by enterprise value cohort since the launch of ChatGPT. The benefits of scale, an entrenched customer base, and most importantly a ton of unique data stands to argue that the larger players will continue to benefit.

When we think about the previous cloud cycle, GS analyst Kash Rangan put together some interesting charts demonstrating that despite the creation of $734B of market cap from new cloud natives, the legacy players excluding Microsoft added 1.5x the amount of market cap. Despite disruption from the new cloud natives like CRM, NOW, and WDAY, the incumbents were able to pivot and take advantage without being completely disrupted (for the most part).

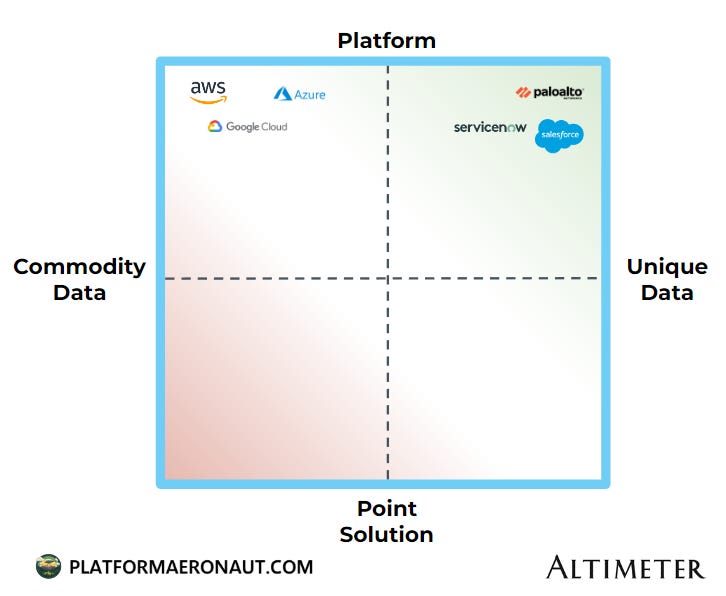

A Framework for Software

It’s becoming increasingly clear that data is incredibly important, but I’d argue that the quality of your data is what can provide a competitive edge with AI for software. Above is a rough framework for one way to think about this with a few sample names in the top two quadrants. I’ll let you do your own work to figure out what may be in the other quadrants.

Commodity vs. Unique Data

If a software provider is going to provide value above and beyond what OpenAI or Anthropic can do it needs to have a competitive moat around data. Commodity data that is generally available and likely fed into an LLM already for training isn’t an edge. The type of customer data that Palo Alto, ServiceNow, and Salesforce contain can feasibly provide an edge using RAG to generate higher quality and more accurate data from AI with fewer hallucinations. We’re already seeing this with NowAssist and Agentforce from ServiceNow and Salesforce respectively.

Arguably despite the hyperscalers having more commoditized data and not truly driving value from the quality of data, the importance of them in terms of infrastructure more than offsets this. When you run an oligarchy it’s fairly hard to be disrupted.

Point Solution vs Platform

In a time of higher scrutiny around IT budgets we’re hearing from CIO and CTOs that the power of a platform is greater than ever. If ServiceNow can offer Customer Workflows that solve problems 90% as good as the point solution but enable budgets to fit into one line item the CTO and CFO are going to take that solution almost every time.

For example let’s take AI Voice Chat. We’re seeing a ton of traction from Bret Taylor’s Sierra and other players like Parloa. But at the same time we’re seeing ServiceNow, Salesforce, and every call center software company start to provide that same service. There’s healthy debate on the startup vs incumbent when it comes to point solutions for emerging technologies.

I’m more focused on the existing point solutions that aren’t AI native. The time for point solutions masquerading as independent companies is likely over as the big players continue to get bigger and offer more services. This is part of the reason we’ve continued to see an explosion in offerings from every large enterprise software company (Workday getting into financial management, Twilio into CDP, ServiceNow into HR+Finance).

What AI Solutions provide a Durable Moat vs Commodity?

We’ve seen a proliferation of “AI” tools and offerings from software companies, but what is actually valuable vs likely to be commoditized? Here’s my swag at what this looks like:

If the backbone of your AI product is off simple tools like Email/SMS generation, Form autofill, or a knowledgebase assistant it’s highly unlikely that is a sustainable moat that a company is able to generate incremental revenue off of.

I’ve spent 15 years analyzing the most hyper-competitive market there is: airlines. If there’s one takeaway it’s that products, features, and services that any competitor can and will provide it ends up being commoditized and just the cost of doing business. Think of wifi on airplanes. Certainly there was a benefit for the first movers to provide Gogo ATG technology on their aircraft, but management teams were promising that the $30/flight of revenue was sustainable. Fast forward and every airline has wifi, it’s constant jockeying for speed and reliability, and there is absolutely zero evidence that incremental revenue has ever been provided to airlines that drops to the bottom line.

On the opposite end of the spectrum, players like ServiceNow, Microsoft, and Salesforce can tangibly provide Autonomous Agents. Palo Alto and Crowdstrike can provide AI enabled Data Security. These solutions are complex, high value, and have a reasonable moat around the products that is driven by proprietary customer data that those companies own. A startup with 20 employees or a subscale $5B market cap software company will find it increasingly difficult to provide the same solution. That moat can result in durable increased profitability.

Enterprise AI Pricing Strategies

If we take a quick sampling of how software companies are pricing their AI solutions today there’s a few different buckets.

AI Features on All Paid Accounts

Klaviyo and Zoom are just giving away their AI solutions to all paying customers. It’s obviously a super easy GTM motion with high adoption. I suspect that the reason this is the case is that their solutions solidly fit in the zone of commoditization today. Both likely have products in the pipeline that progress towards a durable moat, but you don’t have to worry about consumption vs seat and upselling today and can increase your retention and potential new customers but just being quick to market in an easy to adopt fashion.

SKU Gated Upsell Strategy

Monday and Box are providing all their AI features with their top SKUs, it’s an easier sell to just tell customers you can pay an extra 40-60% and get all the AI features plus better core product features. There are some consumption charges at the super high end power user side for these, but generally it’s easy for customers to understand. ServiceNow and Salesforce have their AI solutions SKU gates (ServiceNow requires Pro Plus which is a 60% upcharge) but there’s also some more tangible consumption charges.

Add-On Charges

Adobe and Braze have taken the approach of just doing an add-on charge. It’s easier to tack on $4.99 for Adobe Firefly and have customers opt-in that way than to completely renegotiate contracts.

Consumption Charges

HubSpot is doing the harder but potentially more profitable idea of just doing consumption charges. It costs $0.30 per AI action and although it ties value creation directly to revenue received, there’s still a lot of uncertainty around how customers budget for this.

All of the Above

ServiceNow and Salesforce are tackling the hardest GTM motion of doing almost all of the above. A combination of SKU upgrades, add-on charges, and consumption charges. It’s hard and complex to sell to customers, but every software management team wants to work towards the holy grail: receiving revenue for value delivered. The big question mark for seat-based software is that if AI means you can do 5x the work with 50% of the seats, is that bad for software? By moving towards consumption models, software encumbents can better align their value delivered with revenue received. The difficult thing is it’s going to be messy and uncertain and disruptive.

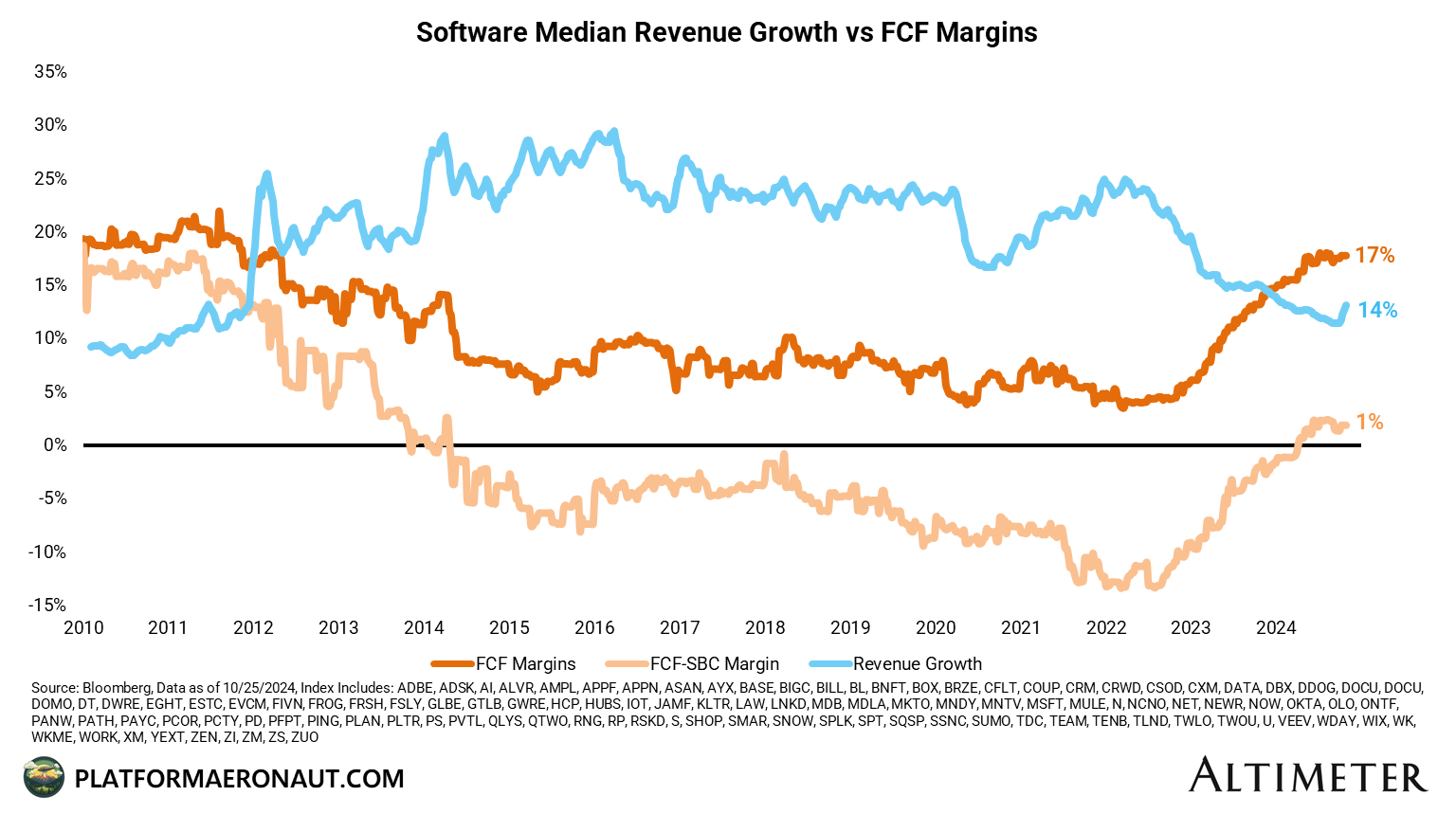

How does this all impact company margins?

Post-ZIRP the software industry has finally gotten back to FCF margins where we were back in 2010-2011 (albeit at significantly lower FCF-SBC margins). There’s been a ton of rationalization and push towards profitability and now layer in AI disruption and opportunity on top of that.

Bottom Line Expenses

You should expect to see a reduction in costs and an increase in productivity and efficiency from AI. Every company, not just software, will be able to benefit from code co-pilots, GTM sales agents, customer service agents, internal search tools like Glean, and more to help drive productivity. Combine that with overhiring, excessive SBC, and a lack of profit focus that is still working it’s way through the system and you can paint a picture of margin expansion through the bottom line.

Top Line Revenue

The bigger question mark for software is around top line acceleration from AI products and services. Larger enterprises like ServiceNow and Salesforce with unique data and platform solutions will likely earn at least their fair share of AI revenues, but there’s big questions around the transition from seat based pricing to consumption based or value provided.

You can envision a scenario where the big get bigger and expand margins both from expense efficiency and unique high-value AI products like NowAssist or Agentforce while at the same time the long-tail of subscale software companies struggle to compete and see commoditization hurt their top line.

Tickers Mentioned: CRM 0.00%↑ SNOW 0.00%↑ MSFT 0.00%↑ PANW 0.00%↑ NOW 0.00%↑ PATH 0.00%↑ WDAY 0.00%↑ NOW 0.00%↑ AMZN 0.00%↑ GOOGL 0.00%↑ U 0.00%↑ BOX 0.00%↑ MNDY 0.00%↑ ZM 0.00%↑ KVYO 0.00%↑ HUBS 0.00%↑ BRZE 0.00%↑ ADBE 0.00%↑

The information presented in this newsletter is the opinion of the author and does not necessarily reflect the view of any other person or entity, including Altimeter Capital Management, LP ("Altimeter"). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation. Past performance is no guarantee of future performance. Altimeter is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

@thomas how does Altimeter define "software returns" in the chart below "Does Scale Matter?" Is is that ROE, ROA, ROIC, etc?

Great piece Thomas